Kalshi Arbitrage: How to Find Real Cross-Venue Price Gaps

Learn how Kalshi arbitrage works, where cross-venue prediction market spreads fail, and how to verify rules, depth, fees, and timing.

Kalshi arbitrage is a cross-venue price gap between Kalshi and another prediction market, often Polymarket. Use a scanner to find candidate pairs, then verify market wording, resolution rules, bid-ask spread, available size, fees, slippage, and timing risk before treating the spread as real.

- A visible spread is only a lead until both legs are executable.

- Rules, resolution source, deadline, and order book depth decide whether a hedge is real.

- Use the Predicts.Guru Arbitrage Scanner for discovery, then verify both venues manually.

- Small spreads can disappear after fees, slippage, partial fills, and timing risk.

What is Kalshi arbitrage?

Kalshi arbitrage is potential profit from a price gap between a Kalshi event contract and a matching market on another venue, often Polymarket. The usual setup is buying YES where it is cheap and buying NO where the opposite side is cheap, with the combined executable cost below the payout. A visible spread is only a lead, not a guaranteed trade.

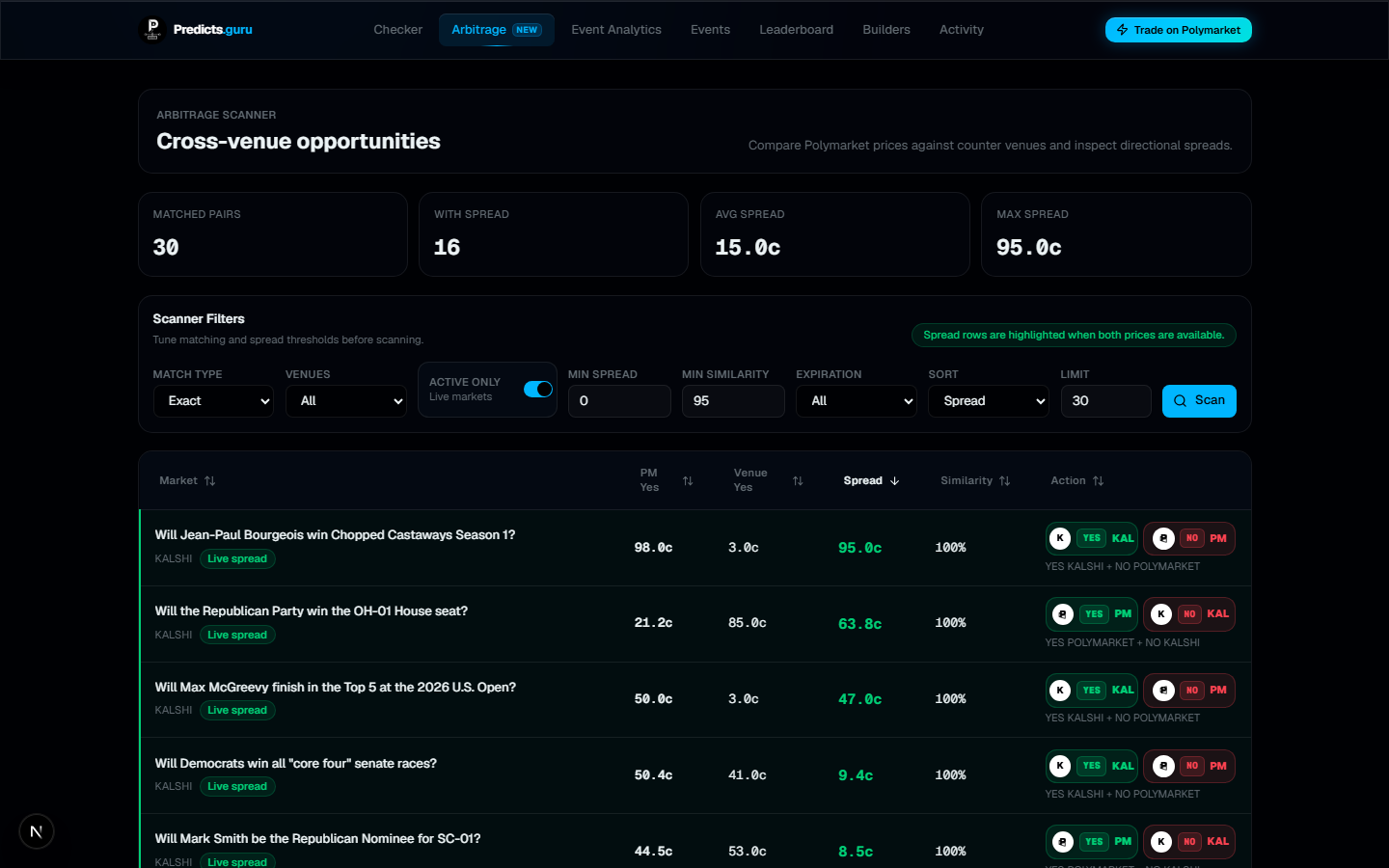

Before acting, verify: Use the Predicts.Guru Arbitrage Scanner to find cross-venue leads, then check both market pages manually.

- Market wording and resolution rules

- Bid/ask spread and available size

- Fees, slippage, and failed-fill risk

- Expiration time and settlement source

- Account access and regional restrictions

Why does Kalshi arbitrage look easier than it is?

Kalshi arbitrage looks simple because binary markets have clean prices. If one market shows YES at 44 cents and another venue lets you buy the opposite side at 53 cents, the math appears to leave 3 cents of spread. That is only the starting point.

The real question is whether both legs can be entered at those prices, in enough size, under matching settlement criteria. Manually checking Kalshi, Polymarket, and other prediction markets is slow. It is also easy to mistake a headline price for an executable price.

A real cross venue arbitrage candidate needs four things at once: Kalshi's own help materials tell traders to read each market's rules before trading because market-specific rules define the criteria, verification source, and procedures for resolution. Polymarket's docs make the same point in a different way: the market title describes the question, but the resolution rules define how it resolves.

That is where many Kalshi price differences break. A spread can be real as a screen result and still fail as a trade.

- The markets must ask effectively the same question.

- The outcomes must resolve in opposite directions.

- The order books must support the size you want.

- The net cost after fees, spread, and slippage must still be below the expected payout.

What counts as real Kalshi arbitrage?

Real Kalshi arbitrage exists when two positions create a defined payout profile across the same real-world event, and the total executable cost is less than the payout after costs. A practical rule of thumb: Executable YES cost + executable NO cost + fees + expected slippage must be below the guaranteed payout.

In most simple binary event markets, that payout is $1.00 per complete YES/NO hedge if the markets truly match. If the all-in cost is $0.98, there may be a 2 cent gross edge. If the all-in cost is $1.01, there is no arbitrage even if the headline prices looked attractive.

The basic YES/NO math

Binary prediction markets usually price outcomes between $0.00 and $1.00. Kalshi explains prices as market-assigned probabilities, where a 70 cent YES contract implies roughly a 70% market probability and a complementary NO side near 30 cents. Polymarket's prices and order book documentation describes a similar probability interpretation for shares.

A hypothetical YES NO prediction market arbitrage example: This example is not live pricing. It is only the arithmetic.

Now pressure-test it: A 3 cent apparent spread can disappear quickly. If fees and slippage cost 2 cents and one leg only fills halfway, the trade may no longer have the shape you intended.

| Leg | Venue | Action | Price |

|---|---|---|---|

| 1 | Kalshi | Buy YES | $0.44 |

| 2 | Polymarket | Buy NO | $0.53 |

| Combined cost | $0.97 | ||

| Maximum payout if markets match | $1.00 | ||

| Gross spread before costs | $0.03 |

- Are those prices asks, bids, or displayed midpoint prices?

- Can you fill both legs at the quoted size?

- Does either venue charge fees on this market?

- Would slippage move the second leg after the first leg fills?

- Do both markets use the same deadline and source of truth?

- Can either market resolve 50/50, be cancelled, or settle under different edge-case rules?

Why same event does not always mean same market

The biggest mistake in polymarket kalshi arbitrage is assuming that similar market titles mean identical contracts. These pairs can look close but behave differently: That difference can turn a hedge into two unrelated bets.

Before pairing two markets, compare: For active traders, this is not a small legal detail. It is the core of the trade.

| Same-looking pair | Hidden mismatch | Why it breaks the hedge |

|---|---|---|

| "Will Candidate A win?" vs "Will Candidate A be declared winner by Source X?" | Different settlement source | One can resolve before or after the other |

| "Will Team B win?" vs "Will Team B win in regulation?" | Different game condition | Overtime can change one result but not the other |

| "Will inflation be above 3%?" vs "Will the first official CPI release show inflation above 3%?" | First release vs later data | Revised data may not count in one market |

| "Will X happen by June 30?" vs "Will X be announced by June 30?" | Event date vs announcement date | The event and announcement can occur on different days |

- Exact title

- Full rules summary

- Resolution source

- End date and timezone

- Treatment of delays, cancellations, and revisions

- Whether the market can resolve as 50/50 or unknown

- Whether one side depends on an announcement rather than the event itself

The Predicts.Guru Arbitrage Scanner is designed to scan matched prediction markets and surface cross-platform price differences between Polymarket, Kalshi, and supported counter venues such as Limitless. It shows matched market pairs, current YES prices, estimated spread, similarity score, expiration context, and action legs to inspect. Use it as a research layer, not as an autopilot.

A disciplined workflow looks like this: The scanner saves time because it reduces the number of markets you need to check manually. It does not replace manual verification.

- Start with exact or high-similarity matches.

- Keep the scan focused on active markets.

- Sort by spread to find the largest apparent gaps.

- Open both action legs in separate tabs.

- Compare the full market wording, not only the title.

- Check expiration and resolution criteria.

- Inspect order book depth on both venues.

- Recalculate the net spread using executable bid/ask prices.

- Confirm fees, account access, and market availability.

- Decide whether the remaining edge is worth the execution risk.

A prediction market arbitrage scanner is strongest at discovery. The trader still owns validation.

1. Match the market rules

Start with the boring part: read the rules. On Kalshi, review the market rules, rules summary, outcome criteria, and verification source. On Polymarket, read the full resolution rules, including source, end date, and edge cases.

Do not rely only on the market title. If the title says "Will X happen?" but the rules say "according to Source Y by Time Z," the source and deadline are part of the trade.

2. Use executable prices, not headline prices

Polymarket's documentation explains that displayed prices may reflect the midpoint of the bid/ask spread, while actual buying usually happens at the ask and selling at the bid. Kalshi's order book help page also shows bids and asks as resting orders at specific prices and quantities. For arbitrage math, midpoint prices are not enough.

Use this structure: If the remaining spread is tiny, execution quality matters more than the original signal.

| Item | Example |

|---|---|

| Buy YES ask | $0.44 |

| Buy NO ask | $0.53 |

| Gross combined cost | $0.97 |

| Estimated fees | $0.01 |

| Expected slippage | $0.01 |

| Net combined cost | $0.99 |

| Remaining spread | $0.01 |

3. Check order book depth

A market can show an attractive price for only a few contracts. Example:

The first 15 or 20 contracts may look profitable. A larger order may not be.

For size, calculate the weighted average fill price. Do not multiply the best price by your full intended position unless the order book actually supports it.

- Kalshi YES ask: $0.44 for 20 contracts

- Next Kalshi YES ask: $0.47 for 400 contracts

- Polymarket NO ask: $0.53 for 15 contracts

- Next Polymarket NO ask: $0.56 for 300 contracts

4. Account for fees and slippage

Kalshi's fees page says fees can vary by market and refers traders to the current fee schedule. Polymarket's fees documentation says fees are determined per market at match time and differ by category.

That means there is no safe shortcut. Check the fee treatment for the exact market and venue before assuming the spread survives. Also include:

The smaller the spread, the more these details matter.

- Spread paid to cross the book

- Partial fills

- Price movement between legs

- Transfer or funding delays

- Withdrawal or deposit constraints

- Tax reporting considerations in your jurisdiction

5. Watch timing risk

Cross venue arbitrage is rarely simultaneous for ordinary users. You may fill one leg, then watch the other venue move before the hedge is complete. This matters most when:

A trade that was positive at the start can become a directional position if only one side fills.

- The market is near resolution

- News is breaking

- Liquidity is thin

- The spread is already small

- One venue has slower funding, withdrawal, or order placement

- Your second leg depends on a manual confirmation step

Kalshi and Polymarket can both be useful in prediction market arbitrage research, but they require different checks.

The point is not that one venue is "better" for arbitrage. The point is that Kalshi vs Polymarket comparisons need contract-level reading. If you skip the rules, the spread is just a number on a screen.

| Factor | Kalshi | Polymarket |

|---|---|---|

| Market type | Event contracts | Prediction market outcome tokens |

| Key check | Market rules and verification source | Resolution rules and oracle process |

| Price check | Order book bids, asks, and contract size | CLOB bid/ask, midpoint, asks, and depth |

| Fee check | Market-specific fee schedule | Per-market fee status and category |

| Access check | Account and jurisdiction eligibility | Platform availability and wallet/funding constraints |

| Arbitrage risk | Rule mismatch, depth, fees, timing | Resolution nuance, depth, fees, timing |

Polymarket leaderboards are useful for context, not proof. A leaderboard can show which traders are active, which markets attract skilled wallets, and where volume or attention is clustering. That can help you spot themes worth scanning, especially if the same market category is active across Kalshi and Polymarket.

But leaderboard performance does not prove a repeatable Polymarket arbitrage strategy. A trader may be winning because of early information, market making, concentrated risk, directional calls, lucky timing, or positions you cannot see in full context. Use leaderboards this way:

Predicts.Guru includes tools beyond the arbitrage page, such as wallet checking, event analytics, and leaderboards, but the same rule applies: market data needs context.

- Identify active market categories.

- Notice traders who repeatedly appear in related events.

- Pair leaderboard research with event analytics and market rules.

- Treat wallet behavior as a clue, not a signal to copy.

- Return to the arbitrage math before placing any trade.

False positive 1: The rules do not match

You find a politics market on Kalshi and a similar one on Polymarket. YES is cheap on one side and NO is cheap on the other. The spread looks attractive.

Then you read the rules.

One market resolves based on final certification. The other resolves based on a named media source before a specific date. If the source calls the result early, delays the call, or changes language, the two markets may not behave as true opposites.

That is not clean arbitrage.

False positive 2: The displayed price is not tradable

A market shows 47 cents, but the best ask is 51 cents. Another venue shows the opposite side at 50 cents, but the available size is small.

The visible spread came from displayed or midpoint prices. The executable spread does not exist.

False positive 3: Liquidity is too thin

The first few contracts create a real spread, but the next level in the book removes it. This can still be useful for very small size, but it is not scalable.

Thin liquidity also increases failed-fill risk. If one side fills and the other side moves, you are left with exposure.

False positive 4: Fees erase the edge

A 2 cent spread can look meaningful. After venue fees, spread paid to cross the book, and a small amount of slippage, it can become zero or negative. For small spreads, do the fee math before celebrating the signal.

False positive 5: Access differs by venue

A market may be visible but not tradable for your account, location, wallet setup, or market status. Prediction market regulation and platform availability can vary by jurisdiction and change over time. Check access before assuming a cross-venue route is available.

Before treating any Kalshi arbitrage opportunity as actionable, run this checklist.

Market match

- Do both markets ask the same economic question?

- Are the deadlines identical?

- Are the timezones clear?

- Is one market about an event while the other is about an announcement?

- Do both markets use compatible settlement criteria?

Rules and resolution

- Have you read the full Kalshi market rules?

- Have you read the full Polymarket resolution rules?

- Do both markets use the same source of truth?

- Are there edge cases that can break the hedge?

- Can either market resolve 50/50, unknown, cancelled, or delayed?

Price and size

- Are you using asks for buys and bids for sells?

- How much size is available at each price level?

- What is the weighted average price for your intended size?

- Would your own order move the market?

- Is the spread still present after realistic fills?

Fees and execution

- What fees apply on each venue?

- Are there maker/taker differences?

- How much slippage should you assume?

- Can both legs fill quickly?

- What happens if only one leg fills?

Operational risk

If any answer is unclear, the result belongs in the research pile, not the trade log.

- Do you have funded accounts on both venues?

- Can you access both markets?

- Are there transfer delays?

- Are you near market expiration?

- Have you considered legal and tax obligations in your jurisdiction?

A spread deserves more attention when several conditions line up: The best candidates are often not the largest displayed spreads. They are the spreads with the cleanest contract match and the most executable liquidity.

A huge spread with weak rule similarity is usually a warning. A smaller spread with clear rules, deep books, and stable prices may be more realistic.

- High similarity between market questions

- Clear, matching resolution criteria

- Meaningful available size on both order books

- Tight bid/ask spreads

- Enough gross spread to survive costs

- No obvious timing or access constraint

- Market not too close to a fast-moving resolution event

Is Kalshi arbitrage risk-free?

No. Even when the math looks hedged, execution risk, rule mismatch, fees, liquidity, access limits, and settlement differences can create losses or remove the edge. Treat "risk-free" claims with skepticism.

Can I use Polymarket arbitrage methods on Kalshi?

Some mechanics carry over, especially YES/NO pricing, implied probability, order book depth, and bid/ask spread checks. The contract details do not carry over automatically. Kalshi and Polymarket can use different rules, sources, and market structures, so every pair needs its own review.

Why do Kalshi and Polymarket prices differ?

Prices can differ because of user base, liquidity, access, fees, market wording, resolution rules, funding constraints, and timing. A price difference may indicate opportunity, but it may also reflect a real difference in contract risk.

What is the fastest way to scan for Kalshi arbitrage?

Use a prediction market arbitrage scanner to find candidate pairs, then manually verify rules, depth, fees, and execution. The Predicts.Guru Arbitrage Scanner is built for that workflow across Polymarket, Kalshi, and supported counter venues.

Kalshi arbitrage is not about finding the biggest number in a spread column. It is about proving that two markets are close enough, liquid enough, and cheap enough to create a real hedge after costs.

Use Predicts.Guru's Arbitrage Scanner to find cross-venue prediction market spreads faster. Then slow down where it matters: read the rules, inspect the order books, calculate the net spread, and confirm that both legs can actually be traded.

A scanner can show you where to look. The trade only becomes real after verification.

Educational content only. Verify live platform rules, fees, availability, and market resolution details before acting.

Check these official Polymarket sources before you act on referral terms, deposit methods, fees, availability, verification, or resolution details.

Last verified: Jun 20, 2026

Find cross-venue prediction market spreads, then verify each pair manually.

Check market wording, movement, liquidity, and rule context before trusting a spread.

Tools and related reading referenced by this guide.

Continue with nearby Polymarket research topics.

Compare Kalshi and Polymarket by access, regulation, market coverage, fees, liquidity, public data, and resolution rules before using either platform.

Compare free Polymarket analytics tools for wallet checks, event research, leaderboards, market context, and public trader discovery.

Learn how to convert Polymarket prices into implied probability, then check spread, liquidity, rules, and wallet context before trusting the signal.